How Gambling Winnings Can Trigger IRS Collections

Winning money from gambling can feel like hitting the jackpot in more ways than one. Whether the money comes from a casino, sports betting, poker tournaments, or an online betting platform, the excitement of a big win can make it feel like easy money.

However, what many taxpayers don’t realize is that gambling winnings are fully taxable income. When those winnings aren’t reported properly on a tax return, it can trigger IRS notices, unexpected tax bills, and eventually IRS collection actions.

At Action Tax Relief we have experience helping taxpayers who find themselves facing IRS tax debt related to gambling winnings. If after reading this blog you still have questions or need help resolving your tax issue, call us at 937-268-2737 or visit www.actiontaxrelief.com.

Gambling Winnings Are Always Taxable

Under federal tax law, gambling winnings must be reported as income on your tax return. This includes winnings from casinos, sports betting, poker tournaments, slot machines, horse racing, online gambling platforms, lotteries, and raffles.

Casinos and gambling institutions often issue Form W-2G, which reports winnings directly to both the taxpayer and the IRS. Even if you do not receive a W-2G, the income is still taxable and must be reported.

The IRS uses computer matching programs to compare third-party reports with what taxpayers report on their returns. When gambling income reported to the IRS does not appear on a tax return, the discrepancy is flagged and the IRS may contact the taxpayer.

The CP2000 Notice: A Common Starting Point

One of the most common notices issued in these situations is a CP2000 Notice, which informs the taxpayer that income reported to the IRS by a third party does not match what was reported on their tax return.

The CP2000 typically proposes additional tax based on the unreported income.

If the notice is ignored or not handled properly, the IRS may assess the additional tax along with penalties and interest. This can include:

- Additional tax on the gambling winnings

- Accuracy-related penalties

- Failure-to-pay penalties

- Interest that continues to accumulate

What started as a gambling win can quickly turn into a growing tax balance owed to the IRS.

When IRS Collections Begin

Once the tax is assessed and the balance remains unpaid, the IRS collection process begins. The IRS sends a series of increasingly serious notices designed to encourage payment.

Typically, the notices progress in stages such as:

- CP14 – The first notice showing the balance due

- CP501 or CP503 – Reminder notices

- CP504 – Notice of intent to levy certain assets

- Letter 1058 or LT11 – Final Notice of Intent to Levy

By the time a taxpayer receives the final notice, the IRS has the legal authority to begin taking aggressive collection actions.

These actions can include wage garnishments, bank account levies, and the filing of a federal tax lien.

Gambling Losses Can Help Reduce the Tax

One important rule many taxpayers overlook is that gambling losses can offset gambling winnings, but only if they are properly documented and reported.

The IRS generally expects taxpayers to keep records such as:

- Betting slips or tickets

- Casino player card statements

- Online betting records

- Bank or credit card records related to gambling activity

Losses can only be deducted up to the amount of winnings and must be claimed as itemized deductions.

In many CP2000 situations, the IRS initially assumes the entire amount of winnings is taxable because losses were not reported on the return. With proper documentation, a tax professional may be able to reconstruct the gambling activity and reduce the tax owed.

The Problem Often Gets Worse Over Time

Another common issue is that taxpayers ignore IRS notices because they are unsure how to respond or believe the problem will resolve itself.

Unfortunately, IRS tax debt rarely goes away on its own. As time passes, penalties and interest continue to accumulate, making the balance larger and harder to resolve.

Even if the IRS has already begun collection actions, solutions are often still available.

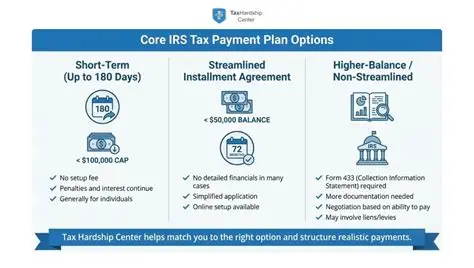

IRS Resolution Options May Be Available

Depending on the taxpayer’s financial circumstances, several IRS resolution options may help resolve gambling-related tax debt, including:

- Installment agreements

- Penalty abatement

- Offer in Compromise

- Currently Not Collectible status

Each case is unique, and the best solution depends on the taxpayer’s financial situation and the details of the tax liability.

Need Help Resolving IRS Tax Debt?

If gambling winnings have triggered IRS notices or collection actions, it’s important to address the problem as early as possible.

Our firm helps taxpayers resolve IRS tax debt, stop collection actions, and negotiate practical solutions with the IRS.

If you owe the IRS because of gambling winnings or any other tax issue, contact Action Tax Relief by calling 937-268-2737 or visiting www.actiontaxrelief.com today to schedule a confidential consultation. The sooner you act, the more options you may have to resolve your tax debt.