by renee | Jun 4, 2026 | Uncategorized

Receiving a notice from the IRS stating you owe additional tax can feel overwhelming. Many taxpayers assume the IRS must be right and simply accept the bill.

But that isn’t always the case.

If you disagree with an IRS determination, whether it involves additional tax, penalties, or certain collection actions, you may have the right to challenge it. Two common options are the IRS Appeals process or filing a case with the United States Tax Court.

Understanding the difference between these options is important because the right strategy can significantly impact the outcome of your case. If after reading this you’re still unsure which path is best, contact Action Tax Relief at 937-268-2737 or visit www.actiontaxrelief.com for help.

What Is the IRS Appeals Process?

The IRS Office of Appeals is an independent division within the IRS that works to resolve disputes between taxpayers and the IRS without going to court.

Appeals Officers review the facts, apply the law, and attempt to reach a fair resolution for both the taxpayer and the government. Many tax disputes are successfully resolved at this stage.

Taxpayers typically enter the Appeals process after receiving notices such as:

• A Notice of Deficiency proposing additional tax

• An audit report they disagree with

• A Collection Due Process (CDP) notice involving liens or levies

• A penalty assessment they believe is incorrect

One of the main advantages of Appeals is that it offers a faster and less formal way to resolve tax disputes without litigation.

Benefits of Resolving a Case Through Appeals

For many taxpayers, the Appeals process offers advantages over going to court. It is generally less formal, faster, and less expensive than litigation, and it allows taxpayers the opportunity to negotiate a settlement and present additional documentation or arguments.

Appeals Officers often consider what are called “hazards of litigation,” meaning they evaluate the strengths and weaknesses of both the taxpayer’s case and the IRS’s position. If there is risk the IRS could lose in court, Appeals may be willing to compromise.

Because of this, many tax disputes are successfully resolved during the Appeals stage.

What Is the U.S. Tax Court?

The United States Tax Court is a federal court where taxpayers can challenge IRS determinations before paying the disputed tax.

When the IRS issues a Notice of Deficiency, taxpayers generally have 90 days to file a petition asking the court to review the IRS decision.

Unlike the Appeals process, Tax Court is a formal legal proceeding. A judge reviews the evidence and applies the tax law to decide the case. Common issues heard in Tax Court include disputed audit adjustments, disallowed deductions or credits, unreported income, and certain penalties.

Once a case is filed, the IRS is represented in court by attorneys from the IRS Office of Chief Counsel.

Key Differences Between Appeals and Tax Court

Both options allow taxpayers to challenge an IRS decision, but they operate very differently.

IRS Appeals:

• Administrative process within the IRS

• Focuses on negotiation and settlement

• Generally faster and less formal

Tax Court:

• Formal judicial proceeding

• Decided by a federal judge

• Requires legal filings and court procedures

In many cases, disputes are resolved through Appeals first. However, if negotiations stall or the legal issues require a judge’s decision, filing in Tax Court may be the better strategy.

Timing Can Be Critical

Timing is an important factor when deciding between Appeals and Tax Court.

For example, if the IRS issues a Notice of Deficiency, taxpayers generally have 90 days to file a petition with the Tax Court. Missing this deadline may eliminate the ability to challenge the determination in court without first paying the tax.

Because IRS deadlines can be strict, it’s important to review your options carefully and respond to notices promptly.

Which Path Is Right for Your Case?

The best path for resolving a tax dispute depends on several factors, including:

• The type of IRS notice received

• The amount of tax involved

• The strength of the legal arguments

• Whether negotiations with the IRS have been productive

In many cases, disputes can be resolved through the Appeals process. In others, filing in Tax Court may be necessary to protect the taxpayer’s rights. Every case is unique, and choosing the right strategy can make a significant difference in the outcome.

Get Professional Help Navigating IRS Disputes

Disputing an IRS determination can be complex, and the decisions you make early in the process can significantly affect the outcome.

Our firm represents taxpayers in IRS disputes, including Appeals conferences and Tax Court cases, helping clients evaluate their options and develop strategies to resolve their tax problems.

If you’ve received an IRS notice or disagree with an IRS determination, contact Action Tax Relief at 937-268-2737 or visit www.actiontaxrelief.com to schedule a confidential consultation.

by renee | Jun 2, 2026 | Tax Resolution

Winning money from gambling can feel like hitting the jackpot in more ways than one. Whether the money comes from a casino, sports betting, poker tournaments, or an online betting platform, the excitement of a big win can make it feel like easy money.

However, what many taxpayers don’t realize is that gambling winnings are fully taxable income. When those winnings aren’t reported properly on a tax return, it can trigger IRS notices, unexpected tax bills, and eventually IRS collection actions.

At Action Tax Relief we have experience helping taxpayers who find themselves facing IRS tax debt related to gambling winnings. If after reading this blog you still have questions or need help resolving your tax issue, call us at 937-268-2737 or visit www.actiontaxrelief.com.

Gambling Winnings Are Always Taxable

Under federal tax law, gambling winnings must be reported as income on your tax return. This includes winnings from casinos, sports betting, poker tournaments, slot machines, horse racing, online gambling platforms, lotteries, and raffles.

Casinos and gambling institutions often issue Form W-2G, which reports winnings directly to both the taxpayer and the IRS. Even if you do not receive a W-2G, the income is still taxable and must be reported.

The IRS uses computer matching programs to compare third-party reports with what taxpayers report on their returns. When gambling income reported to the IRS does not appear on a tax return, the discrepancy is flagged and the IRS may contact the taxpayer.

The CP2000 Notice: A Common Starting Point

One of the most common notices issued in these situations is a CP2000 Notice, which informs the taxpayer that income reported to the IRS by a third party does not match what was reported on their tax return.

The CP2000 typically proposes additional tax based on the unreported income.

If the notice is ignored or not handled properly, the IRS may assess the additional tax along with penalties and interest. This can include:

- Additional tax on the gambling winnings

- Accuracy-related penalties

- Interest that continues to accumulate

What started as a gambling win can quickly turn into a growing tax balance owed to the IRS.

When IRS Collections Begin

Once the tax is assessed and the balance remains unpaid, the IRS collection process begins. The IRS sends a series of increasingly serious notices designed to encourage payment.

Typically, the notices progress in stages such as:

- CP14 – The first notice showing the balance due

- CP501 or CP503 – Reminder notices

- CP504 – Notice of intent to levy certain assets

- Letter 1058 or LT11 – Final Notice of Intent to Levy

By the time a taxpayer receives the final notice, the IRS has the legal authority to begin taking aggressive collection actions.

These actions can include wage garnishments, bank account levies, and the filing of a federal tax lien.

Gambling Losses Can Help Reduce the Tax

One important rule many taxpayers overlook is that gambling losses can offset gambling winnings, but only if they are properly documented and reported.

The IRS generally expects taxpayers to keep records such as:

- Casino player card statements

- Bank or credit card records related to gambling activity

Losses can only be deducted up to the amount of winnings and must be claimed as itemized deductions.

In many CP2000 situations, the IRS initially assumes the entire amount of winnings is taxable because losses were not reported on the return. With proper documentation, a tax professional may be able to reconstruct the gambling activity and reduce the tax owed.

The Problem Often Gets Worse Over Time

Another common issue is that taxpayers ignore IRS notices because they are unsure how to respond or believe the problem will resolve itself.

Unfortunately, IRS tax debt rarely goes away on its own. As time passes, penalties and interest continue to accumulate, making the balance larger and harder to resolve.

Even if the IRS has already begun collection actions, solutions are often still available.

IRS Resolution Options May Be Available

Depending on the taxpayer’s financial circumstances, several IRS resolution options may help resolve gambling-related tax debt, including:

- Currently Not Collectible status

Each case is unique, and the best solution depends on the taxpayer’s financial situation and the details of the tax liability.

Need Help Resolving IRS Tax Debt?

If gambling winnings have triggered IRS notices or collection actions, it’s important to address the problem as early as possible.

Our firm helps taxpayers resolve IRS tax debt, stop collection actions, and negotiate practical solutions with the IRS.

If you owe the IRS because of gambling winnings or any other tax issue, contact Action Tax Relief by calling 937-268-2737 or visiting www.actiontaxrelief.com today to schedule a confidential consultation. The sooner you act, the more options you may have to resolve your tax debt.

by renee | May 28, 2026 | Uncategorized

If you’ve received IRS notices and haven’t taken action, you may be wondering:

Can they really take money from my bank account or even my retirement?

The short answer is yes, and when it happens, it can feel sudden and overwhelming.

At Action Tax Relief we help taxpayers facing bank levies and threatened asset seizures take control and resolve their IRS issues before more damage is done. If after reading this you have questions or need help resolving your tax debt us at 937-268-2737 or visit www.actiontaxrelief.com.

How the IRS Gets to the Point of Seizing Your Money

The IRS doesn’t jump straight to levies. There’s a process. Typically, it looks like this:

- You owe back taxes and don’t pay

- The IRS sends multiple notices requesting payment

- You receive a Final Notice of Intent to Levy (LT11 or Letter 1058)

- You have 30 days to respond or request a hearing

If nothing is done during that 30-day window, the IRS can move forward with enforcement, and that’s when levies come into play.

What Happens When the IRS Levies Your Bank Account

A bank levy is often the first place the IRS goes. Here’s how it works:

Once the IRS issues the levy, your bank is required to freeze the funds in your account, up to the amount you owe. This can include checking and savings accounts.

You don’t lose the money immediately, though. There’s a short window of time (typically 21 days) where the funds are held before being sent to the IRS.

During this time:

- You cannot access the frozen funds

- Any checks or payments you’ve issued may bounce

- Your day-to-day cash flow can come to a halt

If no action is taken, the bank will send the money to the IRS after the holding period.

Can the IRS Take Your Retirement Funds?

This is where things get even more serious, and where many taxpayers are caught off guard.

Yes, the IRS can levy certain retirement accounts, including:

In many situations, the IRS won’t immediately liquidate the account, but they can:

- Seize distributions as they’re paid out

- Force withdrawals under certain conditions

And keep in mind, if funds are withdrawn, you may also face taxes and early withdrawal penalties on top of the IRS levy.

What You Can Do Right Now

If you’re facing a levy or think one is coming, the most important thing is to act quickly.

You still have options, even at this stage.

In many cases, a levy can be:

- Stopped before it happens by responding to the final notice

- Released after it happens if you take immediate action

- Prevented going forward with the right resolution strategy

The IRS is required to release a levy if certain conditions are met, such as proving financial hardship or entering into an acceptable resolution program.

Common Ways to Stop or Remove a Levy

Depending on your situation, there are several paths that may help resolve the issue:

- Installment Agreement: Set up a payment plan to show good faith and stop enforcement

- Currently Not Collectible (CNC): Pause collections if you can’t afford to pay

- Offer in Compromise: Settle your debt for less than the full amount

- Collection Due Process Hearing: Challenge the levy and gain time to resolve

The key is choosing the right option based on your financial situation, not just reacting under pressure.

The Biggest Mistake You Can Make

Waiting too long. By the time a levy hits your bank account, the IRS has already gone through multiple steps to get your attention. Ignoring it further only limits your options and increases the financial damage.

Another common mistake is trying to handle it alone, especially under stress. One wrong move can delay a resolution or make things worse.

Take Back Control Before It Gets Worse

If the IRS has levied your bank account or is threatening to seize your funds, it may feel like you’ve lost control.

But that’s not the case. With the right approach, you can:

- Potentially recover or protect remaining assets

- Put a long-term solution in place

The key is acting fast and having a strategy.

Get a Free Confidential Consultation

If you’re dealing with an IRS levy, or worried one is coming, don’t wait, call Action Tax Relief at 937-268-2737 or visit www.actiontaxrelief.com for a free, no-obligation consultation.

We specialize in helping taxpayers stop IRS collections, protect their assets, and resolve their tax debt the right way.

Don’t let the IRS take control of your finances, take action today.

by renee | May 26, 2026 | Tax Resolution, Tax Resolution

You did the right thing, you filed your taxes. But now you’re facing a balance you can’t afford to pay, and that sinking feeling is real.

If this sounds familiar, you’re not alone and you do have options. The IRS offers programs to help taxpayers resolve their debt, but the key is knowing the right move before you take action.

At Action Tax Relief we have experience helping people navigate tax debt. If after reading this blog you still have questions or need help resolving your tax debt call us at 937-268-2737 or visit www.actiontaxrelief.com.

Let’s walk through five of the most effective ways to deal with IRS tax debt.

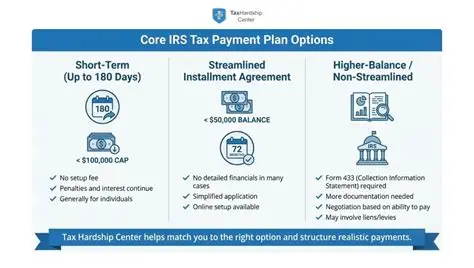

1. Installment Agreements (Monthly Payment Plans)7

The most common solution is an installment agreement. If you can’t pay your balance in full, the IRS will often allow you to set up a monthly payment plan based on what you can afford. Instead of one large payment, you spread it out over time, which can provide immediate relief and help you avoid more aggressive collection actions.

However, not all payment plans are created equal. Some are structured in a way that keeps you paying longer and costing you more in the long run. Others may not fully account for your financial situation.

Bottom line: A payment plan can work, but it needs to be set up strategically.

2. Offer in Compromise (Settle for Less)

You’ve probably heard the phrase “settle your tax debt for pennies on the dollar.” That’s what an Offer in Compromise (OIC) is designed to do, but it’s not as simple as it sounds.

The IRS will only approve an offer if they believe you can’t realistically pay the full amount and that your offer reflects your true ability to pay. When structured correctly, this can significantly reduce your tax debt.

But many taxpayers run into issues by:

- Submitting incomplete or incorrect offers

- Failing to document their financial situation properly

Bottom line: This can be a powerful tool, but only when done right.

3. Currently Not Collectible (CNC) Status

If you truly can’t afford to pay anything, the IRS may place your account into Currently Not Collectible (CNC) status.

This essentially pauses collections and gives you breathing room. While in CNC, the IRS generally won’t pursue aggressive actions like levies, allowing you time to stabilize financially.

Keep in mind, your debt doesn’t disappear, and interest may continue to accrue, but you’re protected from immediate collection pressure.

Bottom line: CNC can provide critical relief when cash flow is tight.

4. Penalty Abatement (Reduce What You Owe)

Many taxpayers are surprised to learn that a significant portion of their balance may be penalties, not just the original tax.

The IRS may reduce or remove penalties if you qualify under certain conditions, such as first-time relief or reasonable cause. This can make a meaningful difference in your total liability.

Instead of assuming the balance is fixed, it’s worth exploring whether part of it can be reduced.

Bottom line: You may not owe as much as you think.

5. Strategic Timing (A Smarter Approach)

Sometimes, the best move isn’t jumping into the first solution available, it’s stepping back and looking at the bigger picture.

The IRS operates under a collection statute (generally 10 years), and timing can play a role in how your case is handled. In certain situations, a more strategic approach can lead to a better overall outcome.

This isn’t something to guess your way through, but it highlights the importance of having a plan.

Bottom line: The right timing can change everything.

The Biggest Mistake to Avoid

Most taxpayers take the first option the IRS offers. That’s a mistake.

The IRS’s goal is to collect as much as possible, as quickly as possible. Your goal should be to resolve your situation in the most favorable way for you, and those two goals don’t always align.

Making the wrong choice can lead to:

- Payments you can’t sustain

- Missed opportunities for better solutions

Take Control Before the IRS Does

If you’ve filed your taxes but can’t pay, the worst thing you can do is ignore it.

The IRS will continue to send notices, and your balance will continue to grow. But with the right strategy, you can take control, reduce what you owe, and move forward with confidence.

Get a Free Confidential Consultation

If you’re dealing with tax debt and unsure what to do next, call Action Tax Relief at 937-268-2737 or visit www.actiontaxrelief.com for a free consultation.

We’ll help you choose the right strategy for your situation. Take control before the IRS does.